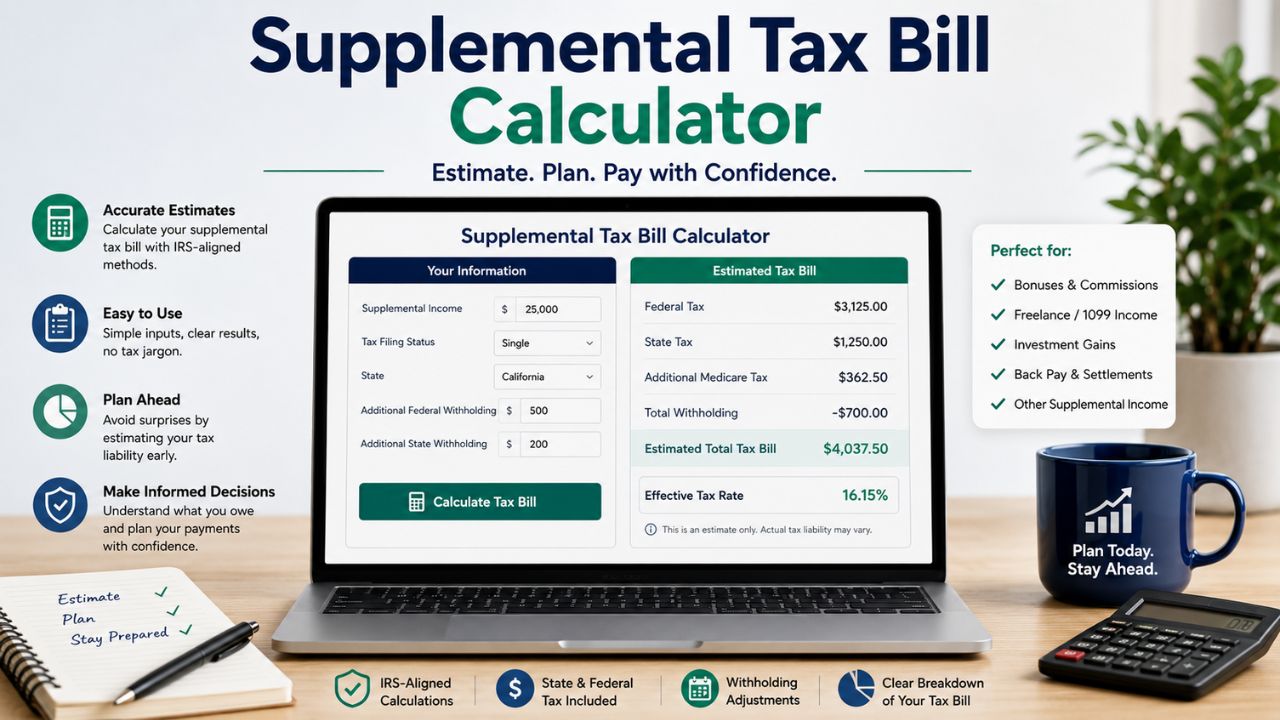

Supplemental Property Tax Calculator

Estimate the one-time supplemental tax bill triggered by a recent property purchase or new construction reassessment.

Estimated Supplemental Breakdown

Estimated Supplemental Tax Due

*Note: This is an estimate. Actual bills are issued directly by your County Tax Collector and may include additional regional flat charges.

Frequently Asked Questions

A supplemental tax bill is a one-time or two-time bill issued when a property undergoes a structural change in ownership or completes new construction. It captures the tax difference between the old assessed value set by the previous owner and your new reassessed value, covering the timeframe from your purchase date to the end of the fiscal tax year.

Usually, no. Most lenders calculate your monthly escrow accounts based strictly on the standard annual tax bill. Because supplemental bills are unique, one-time generation events, they are sent directly to the homeowner. You should contact your lender immediately upon receipt to verify if they will pay it from your escrow overflow or if you must pay it out-of-pocket.

The timeline varies significantly by county workload. Typically, supplemental bills arrive anywhere from 3 to 9 months after your close of escrow date, though it can sometimes take up to a year.

Yes. If you purchase a property for less than the previous assessed value (such as during a market downturn or a distressed sale), the differential is negative. In these cases, the county will issue a supplemental refund check for the prorated overpayment.

Counties operate on a fixed fiscal calendar (often July 1 to June 30). If you buy a house in July, you enjoy the higher valuation for nearly 11 full months of that cycle, meaning you owe 11/12ths of the annual tax difference. If you close in May, you only owe 1/12th because you only owned the property for one month of that tax cycle.

Supplemental bills carry strict legal due dates completely independent of your standard annual property taxes. Failing to pay them by the specified deadline triggers an immediate, mandatory 10% penalty plus additional monthly collection fees.

If you close on a home during the window between March 1st and June 30th, you will likely receive two separate bills. One bill covers the remaining window of the current fiscal year closing out, and the second captures the projection for the upcoming full fiscal year because the rolls were already locked in before your reassessment finished processing.

Yes, supplemental property taxes are treated identically to regular property taxes. If you itemize deductions on federal returns, they are deductible under the SALT (State and Local Taxes) framework up to current statutory caps.

If the property is your primary residence and you qualify for a homestead or homeowners’ exemption, it can be applied to the supplemental calculation to lower the net taxable value differential, provided you file the paperwork within your county’s explicit window post-purchase.

You have the legal right to challenge the assessment. Homeowners typically have 60 days from the mailing date printed on the supplemental notice to file a formal Assessment Appeal with their local county board if they believe the market value calculation is inaccurate.

Understanding Supplemental Reassessments

A supplemental property tax calculation accounts for a common logistical delay in local government accounting. When real estate trades hands, the transaction value instantly resets the asset base for tax purposes. However, the administrative machinery of county tax assessors updates primary assessment rolls on a slower, annual rotation. The supplemental tax statement explicitly covers this lag period.

This calculator functions by identifying the variance between your net acquisition price and the legacy assessed valuation historically carried forward by the county. It multiplies that specific variance by your regional target tax rate to locate your annualized increase. It then looks at your month of closing to apply a prorated fractional modifier based on the remaining calendar allocation of the fiscal tax term. Anticipating this bill keeps new homeowners from experiencing unexpected cash flow issues months after their initial escrow closes.